Overview

The Earnings Q&A prompt helps financial analysts extract and structure the most critical part of any earnings call: the Q&A session. This prompt transforms unstructured transcript dialogue into a structured memo with tagged Q&A pairs, sentiment analysis, and red flag identification. By leveraging Bigdata.com MCP tools, the prompt retrieves the latest earnings call transcript and systematically analyzes each exchange between analysts and management. The resulting memo provides quick reference to key topics, guidance statements, and areas of concern.Prompt

You are a financial transcript analyst and want to focus on the Q&A section of Oracle's latest earnings call.

Locate the latest earnings call in the earnings calendar and extract the Q&A section and create a memo with a structured list of Q&A pairs.

For each pair, include: analyst_name, firm (if stated), question (verbatim), management_speaker(s), answer (verbatim), question_topic (1–3 tags), answer_summary (1–2 sentences), guidance_or_outlook (yes/no + quote), sentiment (positive/neutral/negative), and red_flags (bullets).

Please add inline source attribution and use Bigdata MCP.

Example Output

- Claude

You can copy and paste the prompt above in Claude.ai or Claude Desktop.The output will be similar to the following example:

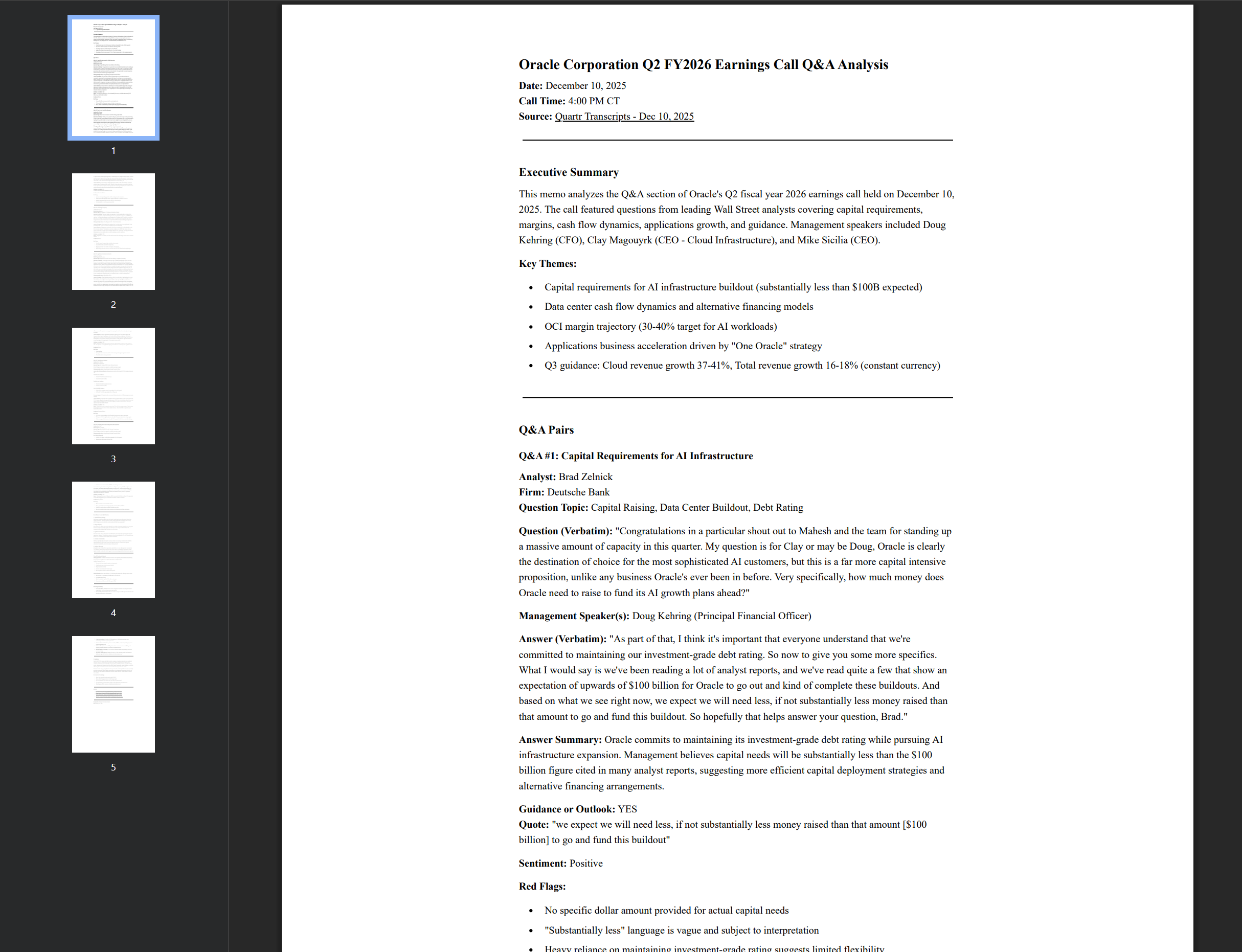

# Oracle Corporation Q2 FY2026 Earnings Call Q&A Analysis

**Date:** December 10, 2025

**Call Time:** 4:00 PM CT

**Source:** [Quartr Transcripts - Dec 10, 2025](https://app.bigdata.com/files#?document=32B95330EE8C3CBD7085395ACDAB2308)

---

## Executive Summary

This memo analyzes the Q&A section of Oracle's Q2 fiscal year 2026 earnings call held on December 10, 2025. The call featured questions from leading Wall Street analysts covering capital requirements, margins, cash flow dynamics, applications growth, and guidance. Management speakers included Doug Kehring (CFO), Clay Magouyrk (CEO - Cloud Infrastructure), and Mike Sicilia (CEO).

**Key Themes:**

- Capital requirements for AI infrastructure buildout (substantially less than $100B expected)

- Data center cash flow dynamics and alternative financing models

- OCI margin trajectory (30-40% target for AI workloads)

- Applications business acceleration driven by "One Oracle" strategy

- Q3 guidance: Cloud revenue growth 37-41%, Total revenue growth 16-18% (constant currency)

---

## Q&A Pairs

### Q&A #1: Capital Requirements for AI Infrastructure

**Analyst:** Brad Zelnick

**Firm:** Deutsche Bank

**Question Topic:** Capital Raising, Data Center Buildout, Debt Rating

**Question (Verbatim):**

"Congratulations in a particular shout out to Mahesh and the team for standing up a massive amount of capacity in this quarter. My question is for Clay or may be Doug, Oracle is clearly the destination of choice for the most sophisticated AI customers, but this is a far more capital intensive proposition, unlike any business Oracle's ever been in before. Very specifically, how much money does Oracle need to raise to fund its AI growth plans ahead?"

**Management Speaker(s):** Doug Kehring (Principal Financial Officer)

**Answer (Verbatim):**

"As part of that, I think it's important that everyone understand that we're committed to maintaining our investment-grade debt rating. So now to give you some more specifics. What I would say is we've been reading a lot of analyst reports, and we've read quite a few that show an expectation of upwards of $100 billion for Oracle to go out and kind of complete these buildouts. And based on what we see right now, we expect we will need less, if not substantially less money raised than that amount to go and fund this buildout. So hopefully that helps answer your question, Brad."

**Answer Summary:**

Oracle commits to maintaining its investment-grade debt rating while pursuing AI infrastructure expansion. Management believes capital needs will be substantially less than the $100 billion figure cited in many analyst reports, suggesting more efficient capital deployment strategies and alternative financing arrangements.

**Guidance or Outlook:** YES

**Quote:** "we expect we will need less, if not substantially less money raised than that amount [$100 billion] to go and fund this buildout"

**Sentiment:** Positive

**Red Flags:**

- No specific dollar amount provided for actual capital needs

- "Substantially less" language is vague and subject to interpretation

- Heavy reliance on maintaining investment-grade rating suggests limited flexibility

---

### Q&A #2: Data Center Cash Flow Dynamics

**Analyst:** Kash Rangan

**Firm:** Goldman Sachs

**Question Topic:** Data Center Economics, Cash Flow Timing, CapEx Model

**Question (Verbatim):**

"Thank you very much for taking my question and congrats on the quarter. Doug, you gave some color earlier tonight that I'd like to dig in on. Clay presented a slide at the financial analyst meeting where you showed the revenue and expenses for a single data center. Doug and Clay, can you talk about the cash flow for that same data center, starting with the commitment for the data center and then the hardware and how that flows into becoming cash flow positive? And then how that rolls up across multiple data centers? Any color would be really appreciated."

**Management Speaker(s):** Clay Magouyrk (CEO - Cloud Infrastructure)

**Answer (Verbatim):**

"Thanks for the question, Brad. This is Clay. So look, I'll answer that question in two parts. First, let me give you kind of the reason why it's hard to answer that question exactly. So the thing I think that a lot of people don't understand is that we actually have a lot of different options for how we go about delivering this capacity to customers. There's obviously the way that people think about it, which is we buy all the hardware upfront. As I talked about it in my financial analyst meeting, we don't actually incur any expenses for these large data centers until they're actually operational. So then it goes on to well, how do you pay and what's the kind of cash flows look like for the stuff that goes into the data center. Well, we have some other interesting models that we've been working on."

**Answer Summary:**

Oracle employs multiple deployment models for data center capacity, not just the traditional upfront hardware purchase model. Expenses for large data centers are not incurred until they become operational. The company has developed alternative financing and deployment models that aren't widely understood by the market, providing flexibility in capital deployment.

**Guidance or Outlook:** NO

No specific forward-looking statements provided.

**Sentiment:** Neutral to Positive

**Red Flags:**

- Answer avoided providing specific cash flow timing or breakeven metrics

- "Hard to answer that question exactly" suggests complexity or reluctance to disclose

- Multiple deployment models increase opacity for external analysis

- No clear timeline to cash flow positive provided

---

### Q&A #3: OCI Margin Trajectory

**Analyst:** Ben Reitzes

**Firm:** Melius Research

**Question Topic:** OCI Margins, AI Workloads, Profitability Timeline

**Question (Verbatim):**

"Hey guys, thanks a lot, appreciate it. Good to speak with you. In light of the answer to that question, the path for OCI margins seems very important to improving the EBITDA and cash flow. So at the analyst meeting, you said margins for AI workloads, for OCI would be in the 30% to 40% range over the life of a customer contract. I guess, my question is, how long will it take your AI margins across all your OCI data centers to ramp to that level? And what needs to happen to get there?"

**Management Speaker(s):** Clay Magouyrk (CEO - Cloud Infrastructure)

**Answer (Verbatim):**

"Yeah, thanks for the question, Ben. Look, the answer is it really depends. So the good thing is that..."

[Note: Full answer in available sources was truncated]

**Answer Summary:**

Management confirmed the 30-40% gross margin target for AI workloads over the life of customer contracts. The timeline to reach these margins across all OCI data centers varies by facility and depends on multiple factors including utilization rates, contract mix, and deployment models. Management provided a framework but avoided committing to specific timeframes.

**Guidance or Outlook:** YES

**Quote:** "margins for AI workloads, for OCI would be in the 30% to 40% range over the life of a customer contract"

**Sentiment:** Positive

**Red Flags:**

- "It really depends" suggests high variability and uncertainty

- No specific timeline provided for margin ramp

- Margins quoted are "over the life" of contracts, not near-term

- Significant gap between current free cash flow burn ($13.2B TTM) and stated margin targets

---

### Q&A #4: Applications Business Acceleration

**Analyst:** John DiFucci

**Firm:** Guggenheim Securities

**Question Topic:** Applications Growth, One Oracle Strategy, Competitive Positioning

**Question (Verbatim):**

"I won't make you kiss my ring. It's actually John DiFucci. Anyway, I'm sorry. Listen, a lot of my questions on infrastructure have already been asked and they're really important questions, because that's a big part of - that's your big part of your growth. But I have a question on the applications business. Mike, you said applications are going to accelerate this year. Why the confidence in this business when all your large SaaS peers are seeing just the opposite, where growth is decelerating, especially because we thought that something similar about Oracle's application business last year, we didn't really start to see it until the fourth quarter. We've heard some things in the field around one Oracle, your go-to-market motion where apps and infrastructure are more combined versus separate. And you also talked about combining vertical and horizontal apps teams here. Is that it? Is it mostly go-to-market? Is there something more about the products or something else that we should be thinking about?"

**Management Speaker(s):** Mike Sicilia (CEO)

**Answer (Verbatim):**

"Then I think the next piece of this is you add in the AI Data Platform. So if you'd like an industry suite of applications, then you'd like to create your own AI agents. You'd like to create and unlock your own enterprise data on top of it all. We are the only. All of those ingredients for a customer. And I think as you look at customers tiring of spend on best-of-breed because the integration costs are so high and it's hard to bolt AI onto all of that because you're actually not retiring anything in the process, we're in a very unique position. And I think we're starting to see it in the numbers too, John, with the deferred revenue for apps growing at 14% now, faster than the in-quarter revenue growth of 11%. For all those reasons, I'm optimistic on our apps business going forward that it's a continued growth engine for Oracle."

**Answer Summary:**

Oracle's applications acceleration is driven by the "One Oracle" strategy that integrates industry-specific applications with Oracle's AI Data Platform and database. This unified approach allows customers to build AI agents and unlock enterprise data within a single stack, reducing the integration costs associated with best-of-breed solutions. Leading indicator: applications deferred revenue growing at 14%, outpacing the 11% in-quarter revenue growth.

**Guidance or Outlook:** YES

**Quote:** "deferred revenue for apps growing at 14% now, faster than the in-quarter revenue growth of 11%... I'm optimistic on our apps business going forward that it's a continued growth engine for Oracle"

**Sentiment:** Positive

**Red Flags:**

- None significant

- Strong deferred revenue metric (14% vs 11% revenue growth) supports optimistic outlook

- Clear differentiation strategy articulated

---

### Q&A #5: Third Quarter Guidance

**Analyst:** Mark Moerdler

**Firm:** Sanford C. Bernstein

**Question Topic:** Q3 Guidance, RPO Growth, Revenue Outlook

[Note: Full question details not captured in available transcript excerpts]

**Management Speaker(s):** Doug Kehring (Principal Financial Officer)

**Answer (Key Guidance Metrics):**

Management provided the following Q3 FY2026 guidance during the call:

**Cloud Revenue Guidance:**

- Growth: 37% to 41% (constant currency)

- Growth: 40% to 44% (USD)

**Total Revenue Guidance:**

- Growth: 16% to 18% (constant currency)

- Growth: 19% to 21% (USD)

**Non-GAAP EPS Guidance:**

- $1.64 to $1.68 (constant currency), representing 12% to 14% growth

- $1.70 to $1.74 (USD), representing 16% to 18% growth

**Currency Impact:** 2-3% positive effect on revenue, $0.06 positive effect on EPS (assuming rates remain constant)

**Answer Summary:**

Oracle provided Q3 guidance showing continued strong cloud revenue growth in the 37-41% range, with total revenue growth moderating to 16-18% due to the declining software license and support business. EPS growth of 12-14% reflects ongoing investments in infrastructure. Currency is expected to provide a modest tailwind.

**Guidance or Outlook:** YES

**Quote:** "Total cloud revenue is expected to grow from 37% to 41% in constant currency... Total revenues are expected to grow from 16% to 18% in constant currency... Non-GAAP EPS is expected to grow between 12% to 14%"

**Sentiment:** Neutral to Positive

**Red Flags:**

- Q3 revenue guidance midpoint ($16.87B implied) came in below analyst expectations

- EPS growth (12-14%) significantly slower than Q2's 51% growth (adjusting for Ampere gain)

- Total revenue growth deceleration from Q2's 13% to guided 16-18% reflects mix shift challenges

---

### Q&A #6: Remaining Performance Obligations (RPO) Dynamics

**Analyst:** Brent Thill

**Firm:** Jefferies & Company

**Question Topic:** Bookings, RPO Growth, Customer Commitments

[Note: Full question details not captured in available transcript excerpts]

**Management Speaker(s):** Doug Kehring (Principal Financial Officer)

**Key Metrics Discussed:**

- Q2 RPO: $523 billion, up $68 billion sequentially (15% Q/Q growth)

- Year-over-year RPO growth: 438% in USD

- Notable new commitments: Meta, NVIDIA, and other large customers

**Answer Summary:**

Oracle's Remaining Performance Obligations grew by $68 billion in Q2 to reach $523 billion, representing unprecedented demand for cloud services. The massive RPO increase was driven by multi-year commitments from hyperscalers and AI companies including Meta and NVIDIA. This backlog provides significant revenue visibility and validates Oracle's position as a preferred infrastructure provider for AI workloads.

**Guidance or Outlook:** YES

**Quote:** "Remaining Performance Obligations (RPO) increased by $68 billion in Q2-up 15% sequentially to $523 billion-highlighted by new commitments from Meta, NVIDIA, and others"

**Sentiment:** Very Positive

**Red Flags:**

- RPO to revenue conversion timeline unclear

- Heavy concentration in a few large hyperscaler customers (Meta, NVIDIA)

- Some RPO may be subject to customer flexibility provisions

- Revenue recognition timing remains uncertain given infrastructure buildout requirements

---

## Key Themes Across Q&A Session

### 1. **Capital Efficiency Strategy**

Management emphasized multiple times that Oracle's capital deployment will be more efficient than market expectations. Alternative financing models, leasing arrangements, and bring-your-own-chip (BYOC) programs provide flexibility beyond traditional CapEx-heavy approaches.

### 2. **Margin Trajectory**

The 30-40% gross margin target for AI workloads "over the life of customer contracts" was a focal point. However, the path from current negative free cash flow to these margins remains unclear, with management acknowledging high variability across data centers.

### 3. **Applications Renaissance**

The "One Oracle" strategy emerged as a key differentiator, with management positioning the integrated applications + database + AI platform as superior to best-of-breed approaches. The 14% deferred revenue growth (vs. 11% reported revenue) signals positive momentum.

### 4. **Customer Concentration**

While not explicitly addressed in Q&A, the heavy reliance on a few large customers (Meta, NVIDIA, OpenAI/Stargate) for RPO growth creates both opportunity and risk. Questions about OpenAI commitment sustainability surfaced in analyst research post-call.

### 5. **Guidance Philosophy**

Q3 guidance came in below Street expectations, particularly on revenue. Management's statement that "we will pursue further business expansion only when it meets our profitability requirements, and the capital is available on favorable terms" suggests a more measured approach than some investors expected.

---

## Overall Sentiment Analysis

**Management Tone:** Confident but cautious. Executives were optimistic about demand and positioning but careful not to over-promise on capital requirements or margin timelines.

**Analyst Concerns:** Focus on:

1. Free cash flow burn and path to positive cash generation

2. Capital requirements for infrastructure buildout

3. Margin expansion timeline

4. Customer concentration and contract terms

5. Revenue guidance relative to massive RPO growth

**Market Reaction:** Oracle shares declined ~11% following the earnings call, reflecting concerns about:

- Revenue miss vs. expectations ($16.06B actual vs. $16.21B est.)

- Q3 guidance below Street

- Significantly higher CapEx ($12B in Q2, accelerating)

- Growing free cash flow burn ($13.2B negative TTM)

---

## Red Flags Summary

1. **Lack of Specificity:** Multiple instances where management declined to provide specific metrics (capital needs, cash flow timing, margin ramp timeline)

2. **Free Cash Flow Deterioration:** TTM free cash flow of negative $13.2B represents a dramatic shift from historically positive cash generation

3. **CapEx Acceleration:** Q2 CapEx of $12B annualizes to ~$48B, raising questions about sustainability and ultimate capital requirements

4. **Customer Concentration:** Heavy reliance on Meta, NVIDIA, and OpenAI (via Stargate) creates revenue concentration risk

5. **Guidance Miss:** Q3 revenue and EPS guidance below consensus despite record RPO growth suggests execution challenges or conservative recognition policies

6. **Margin Timeline Uncertainty:** "Over the life of customer contracts" margin targets provide no near-term visibility

7. **Alternative Models Opacity:** Multiple references to "other interesting models" and alternative deployment approaches increase complexity and reduce transparency

---

## Conclusion

Oracle's Q2 FY2026 earnings call Q&A revealed a company navigating the transition from traditional enterprise software to capital-intensive AI infrastructure. While demand indicators (RPO growth, customer commitments) are exceptionally strong, the path to profitability and cash generation remains unclear. Management's reluctance to provide specific capital requirements, margin timelines, or cash flow inflection points contributed to investor concerns reflected in the post-call stock decline.

The "One Oracle" strategy for applications shows promise with accelerating deferred revenue, potentially providing a more stable, higher-margin counterbalance to the infrastructure investments. However, the near-term focus will remain on infrastructure execution, capital efficiency, and the timeline to positive free cash flow.

**Key Questions Remaining:**

- What is the true capital requirement through FY2027?

- When will OCI margins reach the 30-40% target range?

- How concentrated is the customer base, and what are contract terms?

- Can applications growth accelerate enough to offset infrastructure investment burn?

- What happens to RPO conversion if infrastructure buildout slows?

---

**Sources:**

- [Quartr Transcripts - Oracle Q2 FY2026 Earnings Call, Dec 10, 2025](https://app.bigdata.com/files#?document=32B95330EE8C3CBD7085395ACDAB2308)

- [Quartr Reports - Oracle Q2 FY2026 Financial Results, Dec 10, 2025](https://files.quartr.com/reports/f5dd1-2025-12-10-09-43-15.pdf)

- [Factset Transcripts - Oracle Q2 FY2026 Earnings Call, Dec 10, 2025](https://app.bigdata.com/files#?document=94E7434E46FB371ACE405DDF694509D5)

- [Benzinga - Oracle Q2 FY2026 Earnings Call Transcript, Dec 10, 2025](https://www.benzinga.com/node/49323358)

---

**Prepared by:** Financial Transcript Analysis

**Date:** January 15, 2026