Why It Matters

Understanding how countries are exposed to financial contagion and spillover effects from rising bond spreads is critical for sovereign risk assessment and macroeconomic stability analysis. As bond yields diverge and sovereign debt costs increase, policymakers and analysts must proactively assess exposure to financial market tensions, fiscal pressures, and potential contagion effects across Western European nations.What It Does

TheRiskAnalyzer class, part of the bigdata-research-tools package, is purpose-built to meet this challenge. Designed for risk analysts, portfolio managers, and investment professionals, it systematically analyzes entity exposure to specific risk channels using unstructured data from news, earnings calls, and regulatory filings.

How It Works

TheRiskAnalyzer combines hybrid semantic search, risk factor taxonomies, and structured validation techniques to deliver:

- Targeted extraction of risk signals and supporting evidence from massive unstructured datasets

- Standardized exposure metrics to compare risk across different countries

- Actionable insights that inform investment strategies and sovereign bond positioning decisions

- Time-based monitoring to track how exposure levels shift in response to bond market developments

A Real-World Use Case

This cookbook illustrates the full workflow through a practical example: identifying Western European countries facing spillover risks from rising bond spreads. You’ll learn how to convert unstructured narrative (news articles) into structured, quantifiable sovereign risk intelligence, tracking bond market pressures across Germany, France, Italy, Spain, and other European nations. Ready to get started? Let’s dive in!Prerequisites

To run the Rising Bond Spread Risks workflow, you can choose between two options:-

💻 GitHub cookbook

- Use this if you prefer working locally or in a custom environment.

- Follow the setup and execution instructions in the

README.md. - API keys are required:

- Option 1: Follow the key setup process described in the

README.md - Option 2: Refer to this guide: How to initialise environment variables

- ❗ When using this method, you must manually add the OpenAI API key:

- ❗ When using this method, you must manually add the OpenAI API key:

- Option 1: Follow the key setup process described in the

-

🐳 Docker Installation

- Docker installation is available for containerized deployment.

- Provides an alternative setup method with containerized deployment, simplifying the environment configuration for those preferring Docker-based solutions.

Setup and Imports

Below is the Python code required for setting up our environment and importing necessary libraries.Defining Your Risk Analysis Parameters

To perform a sovereign risk analysis, we need to define several key parameters:- Main Theme (

main_theme): The risk scenario to analyze (e.g. Spillovers from Rising Bond Spreads in Western Europe) - Focus (

analyst_focus): The analyst focus that provides an expert perspective on the scenario and helps break it down into risks - Entity Universe (

dict_country_bank,entity_names_countries,entity_names_banks): The set of countries to screen (note: institutional entities are used internally to maximize data coverage) - Control Entities (

control_entities): The set of entities to be always co-mentioned with your watchlist (e.g. people, places, organizations, etc) - Time Period (

start_dateandend_date): The date range over which to run the search - Document Type (

document_type): Specify which documents to search over (transcripts, filings, news) - Sources (

sources): Specify set of sources within a document type, for example which news outlets (available via Bigdata API) you wish to search over - Model Selection (

llm_model): The AI model used for semantic analysis - Rerank Threshold (

rerank_threshold): By setting this value, you’re enabling the cross-encoder which reranks the results and selects those whose relevance is above the percentile you specify (0.7 being the 70th percentile). More information on the re-ranker can be found here.

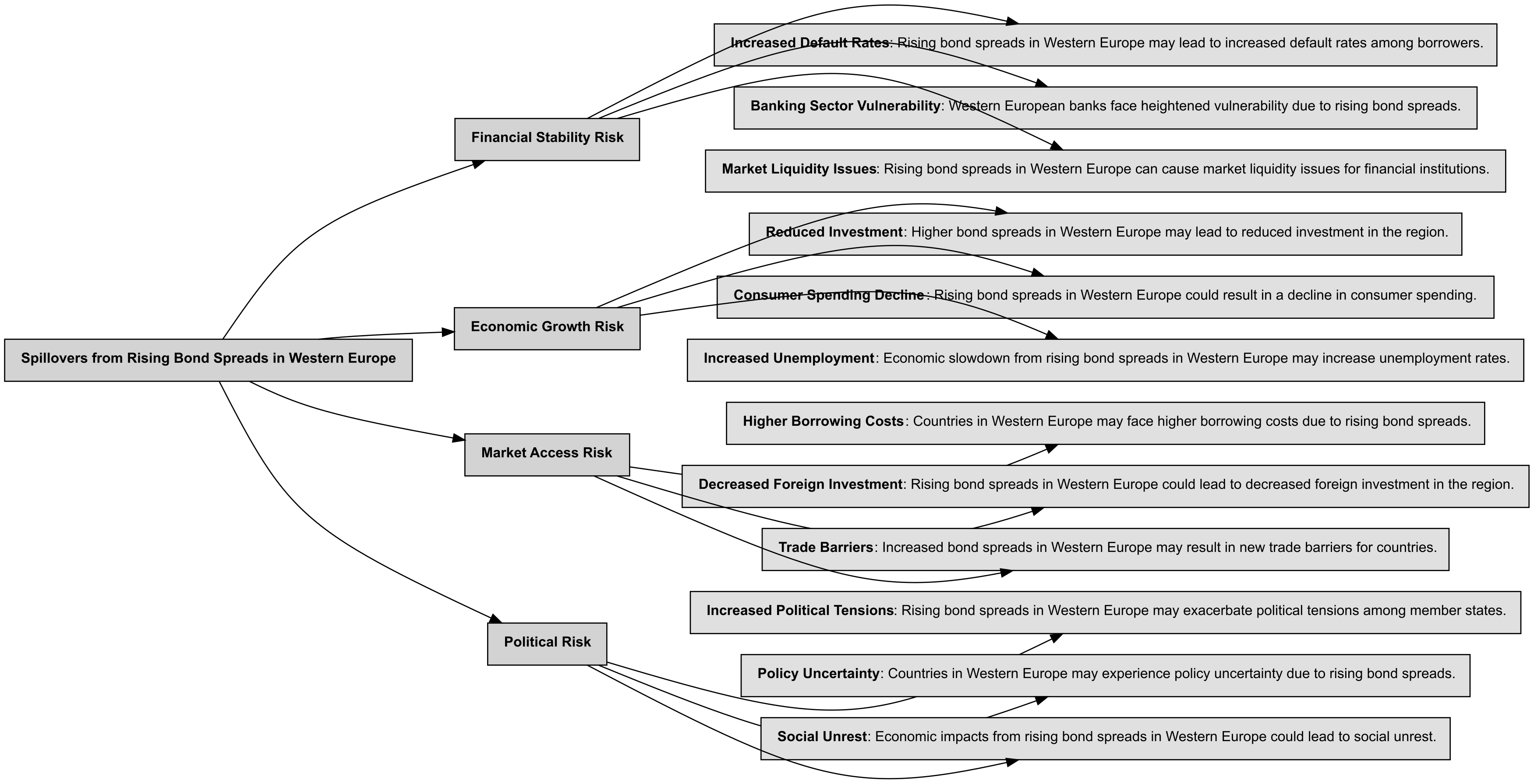

Mindmap a Risk Taxonomy with Bigdata Research Tools

You can leverage Bigdata Research Tools to generate a comprehensive risk taxonomy with an LLM, breaking down the complex bond spread spillover scenario into well-defined risk factors and sub-scenarios for more targeted analysis.

Retrieve Content Using Bigdata’s Search Capabilities

With the risk taxonomy and screening parameters, you can leverage the Bigdata API to run a search on news articles. We need to define 3 more parameters for searching:- Frequency (

freq): The frequency of the date ranges to search over. Supported values:Y: Yearly intervalsM: Monthly intervalsW: Weekly intervalsD: Daily intervals

- Document Limit (

document_limit): The maximum number of documents to return per query to Bigdata API - Batch Size (

batch_size): The number of entities to include in a single batched query

Label the Results

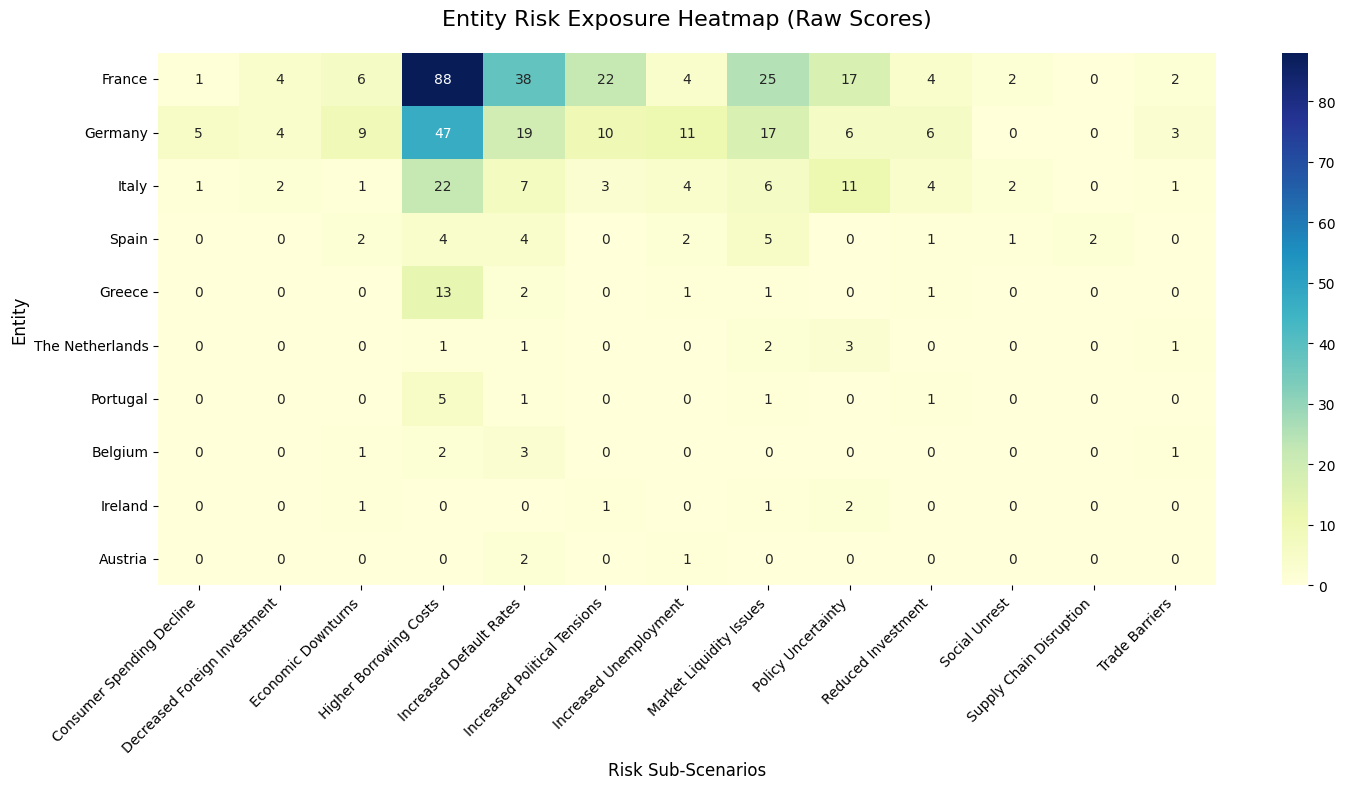

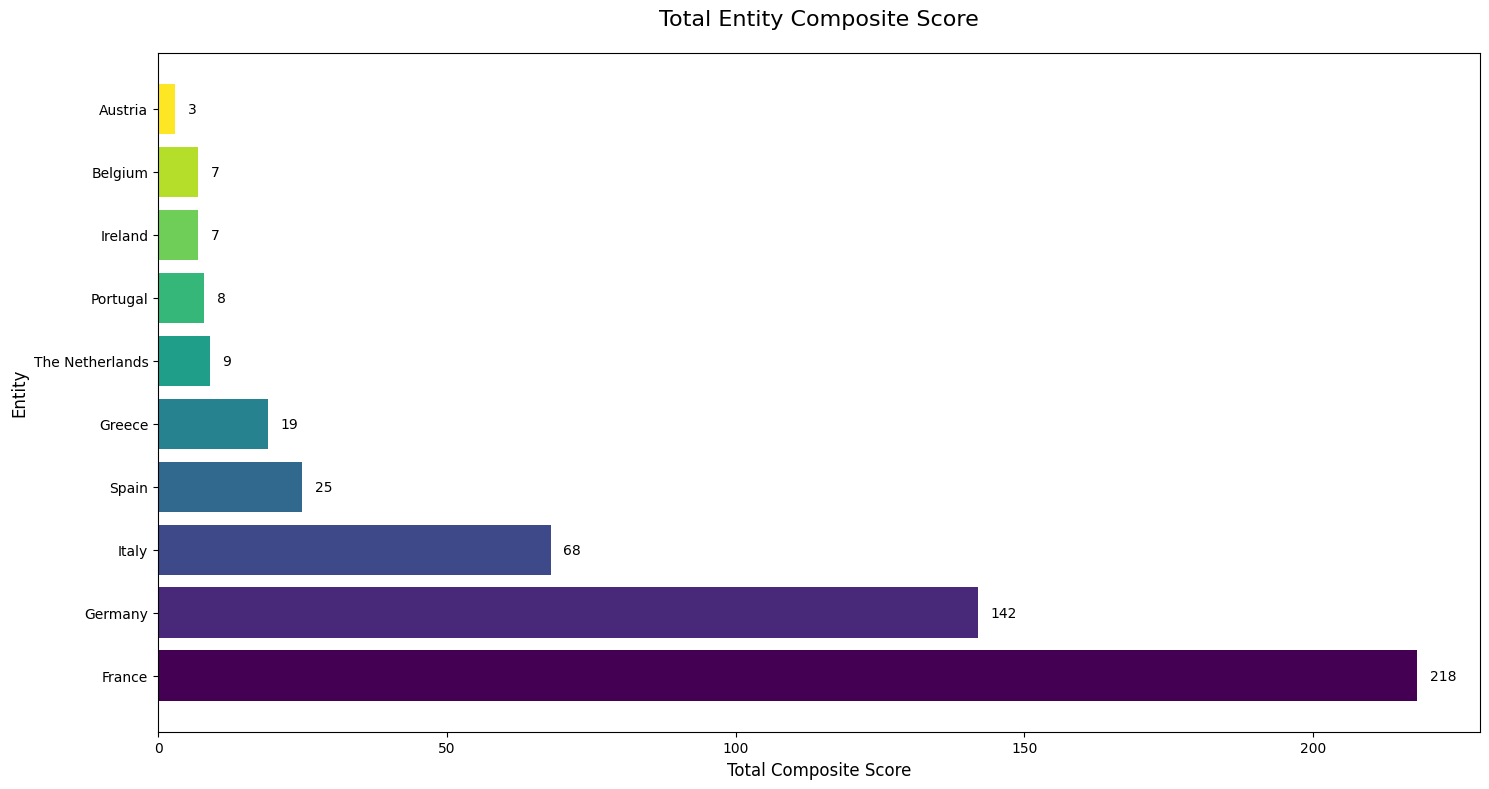

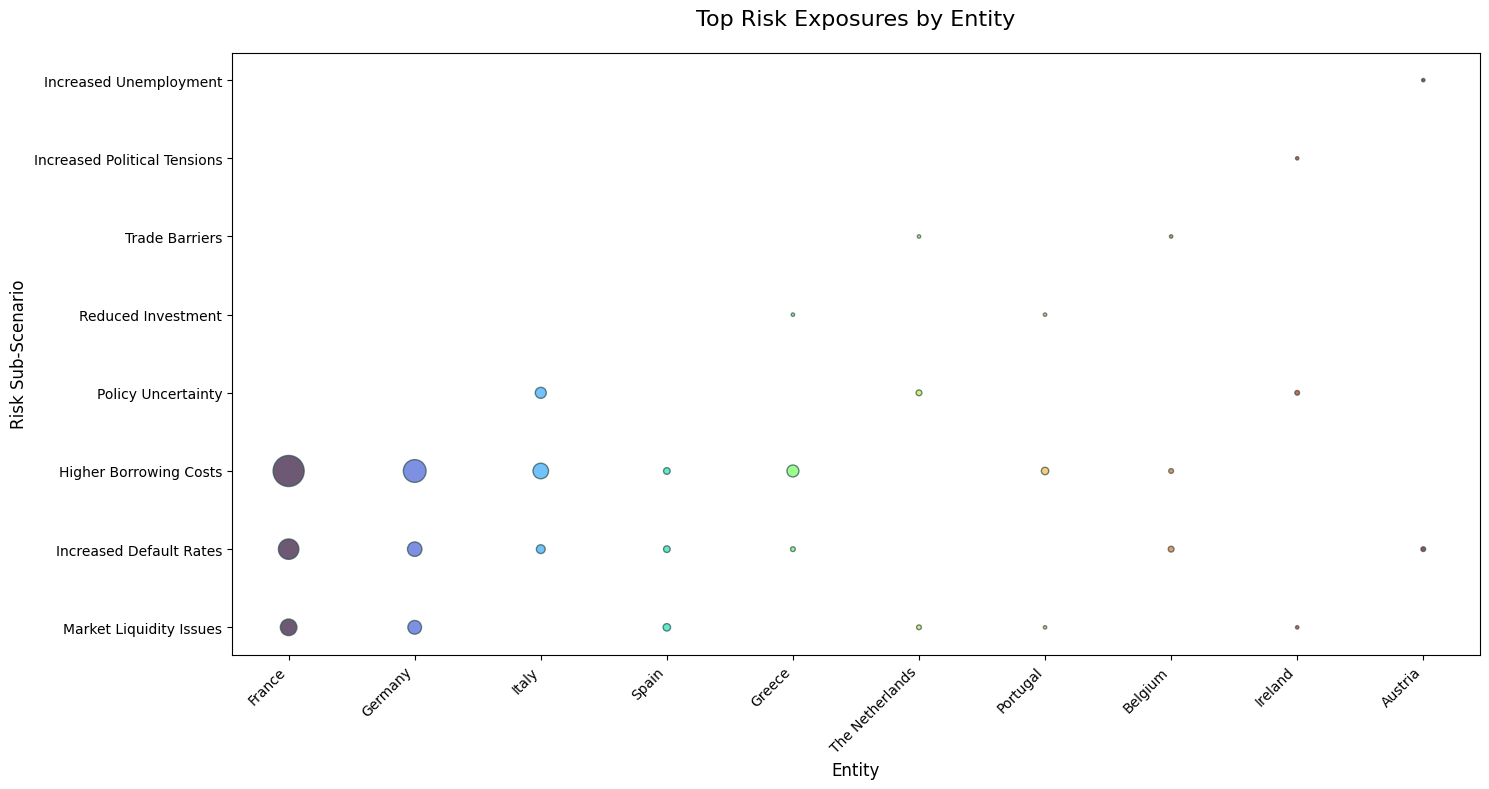

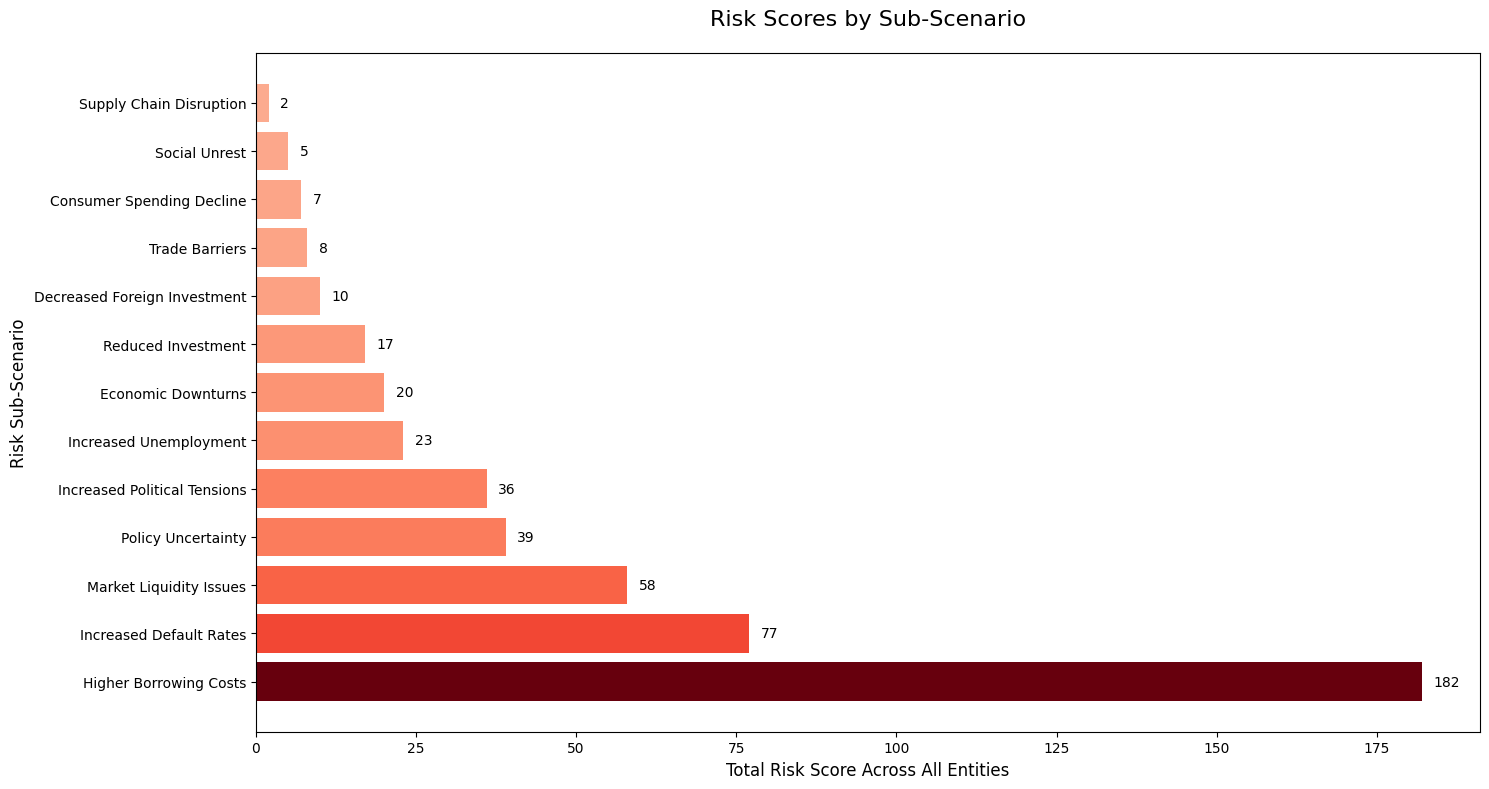

Use an LLM to analyze each text chunk and determine its relevance to the sub-themes. Any chunks which aren’t explicitly linked to our main theme will be filtered out.Assess Country-Level Risk Exposure

The functionget_scored_df will calculate the composite thematic score, summing up the scores across the sub-scenarios for each country (df_entity).

Create Daily Sentiment Indicators

Generates a complete daily time grid for all entities and calculates rolling sentiment indicators (30/90 days), news volumes, and normalized metrics for temporal analysis.Identify Peak Coverage and Sentiment Windows

Identifies time windows of maximum media coverage and most negative sentiment for each country, useful for analyzing critical risk moments.Generate AI-Powered Narrative Summaries

Uses an LLM to synthesize the main narratives in peak windows, providing a qualitative summary of the risks that emerged for each country during the most critical moments.Visualizations

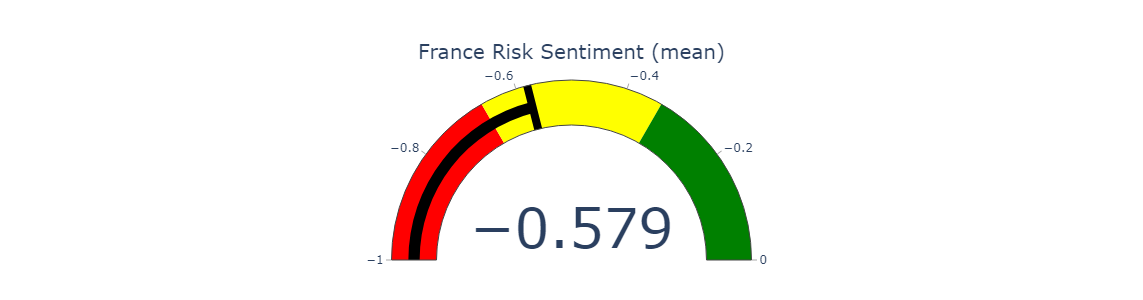

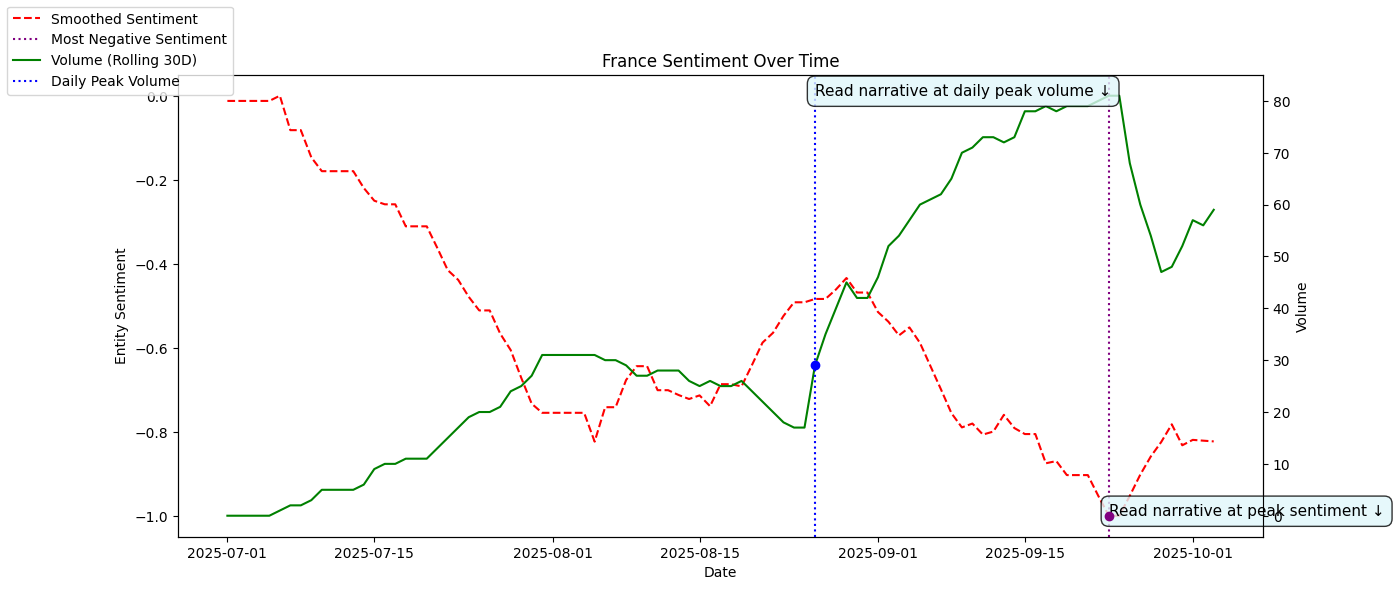

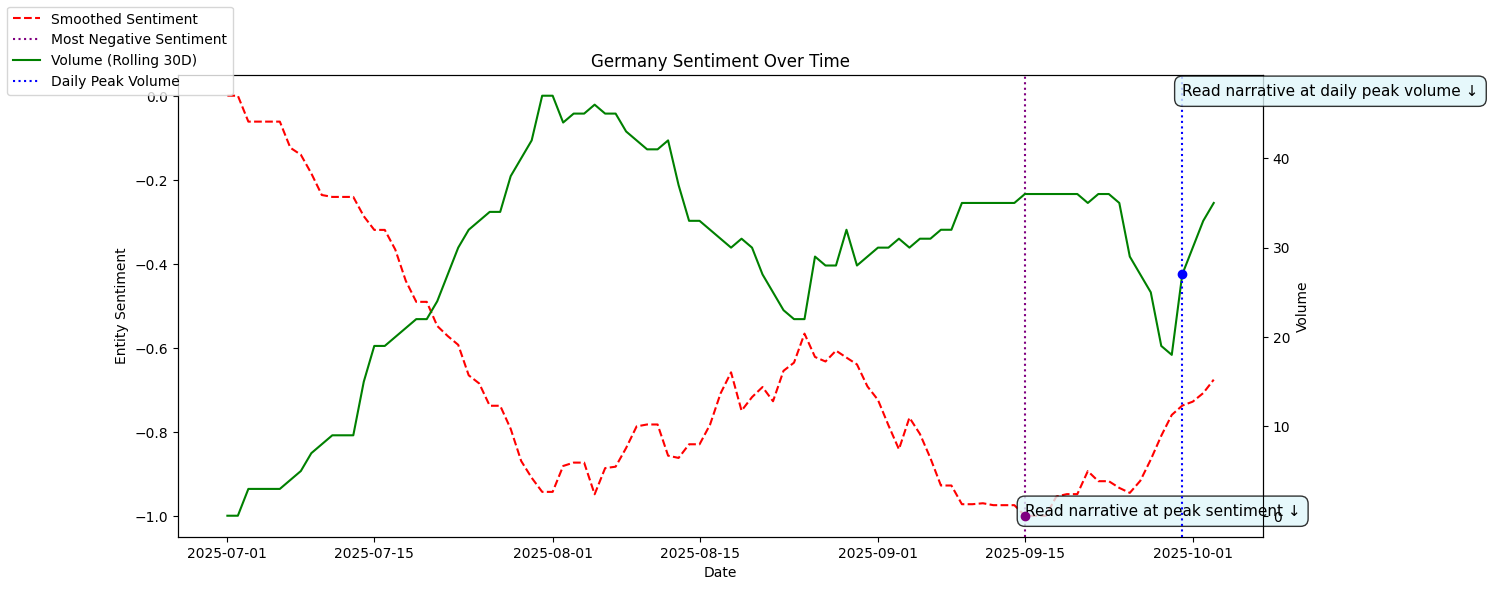

Generates interactive dashboards for each country with sentiment time series charts, gauge indicators, and qualitative narratives at peak coverage or negativity moments. For each country, the analysis produces:- Sentiment Gauge: Visual indicator showing the mean (or minimum not normalized) of the rolling sentiment values over the entire period

- Sentiment Time Series: Rolling sentiment trends over time (30-day rolling window) with rolling volume (30-day) for smoother visualization

- Peak Negative Sentiment Narrative: AI-generated summary of risks during the most negative sentiment period

- Peak Volume Narrative: AI-generated summary of risks during the highest daily media coverage period

Example: France Risk Dashboard

Peak Volume Narrative - Date: 26-08-2025

France is currently facing significant refinancing risk in real estate, exacerbated by a confluence of political instability, rising borrowing costs, and deteriorating investor sentiment. Recent headlines highlight the European Central Bank’s cautious stance amid global trade tensions, with ECB President Christine Lagarde warning of persistent downside risks, including the impact of U.S. tariffs on European economies. The introduction of a 15% tariff on most European goods has led to skepticism about the economic balance of the new EU-U.S. trade deal, with French officials labeling it an act of “submission.” This has contributed to a sharp decline in the euro and heightened concerns over France’s export sectors. Furthermore, the country’s long-term borrowing costs have surged, with yields on 10-year bonds approaching those of Italy for the first time since the financial crisis, reflecting investor anxiety over France’s fiscal sustainability amid a record public deficit and political turmoil. The government’s potential collapse could trigger a further spike in borrowing costs, complicating fiscal consolidation efforts and limiting policy flexibility. As a result, the risk of increased default rates looms large, particularly for the banking sector, which is heavily exposed to government bonds. The combination of these factors signals a precarious outlook for France’s real estate market, as higher financing costs and political uncertainty could stifle investment and economic growth, leading to a potential downturn in property values.

Peak Negative Sentiment Narrative - Date: 23-09-2025

France is currently facing significant refinancing risk in its real estate and broader financial markets, as highlighted by a series of alarming news reports from August and September 2025. The yield on French 10-year bonds has surged to levels surpassing those of historically troubled economies like Greece and Portugal, reflecting a loss of investor confidence amid escalating political instability and a looming government collapse. The yield spread between French and German bonds has widened dramatically, indicating that investors are demanding higher compensation for holding French debt due to concerns over the country’s fiscal sustainability and political gridlock. The government’s inability to implement necessary austerity measures, coupled with a budget deficit projected at 5.8% of GDP, has exacerbated fears of a potential credit rating downgrade, which could further increase borrowing costs. Analysts warn that if the current political turmoil continues, France could find itself on the periphery of the eurozone, with borrowing costs exceeding those of Italy for the first time in decades. This situation poses severe risks not only to France’s financial stability but also to the broader eurozone, as a crisis in France could have spillover effects on neighboring economies. The combination of high debt levels, rising interest rates, and political uncertainty creates a precarious environment for investors, who are increasingly wary of the sustainability of French assets. Immediate actions are needed to restore confidence, including decisive fiscal reforms and political stability, to prevent a deeper crisis that could threaten the viability of the eurozone itself.

Example: Germany Risk Dashboard

Peak Volume Narrative - Date: 30-09-2025

Germany is currently facing significant refinancing risk in its real estate and broader financial markets, as highlighted by a series of concerning developments in September 2025. The yield on Germany’s 30-year bonds has surged to its highest level in over a decade, reaching 3.40%, amid a broader selloff in European bond markets driven by rising public debt and inflationary pressures. This trend is exacerbated by political instability in France, which has led to increased risk premiums on French bonds and a widening spread between French and German yields, now at its highest since the Eurozone debt crisis. The implications for Germany are severe; as the country prepares to issue new government bonds to finance its spending, the elevated borrowing costs could strain public finances and hinder economic recovery efforts. Additionally, rising unemployment, which recently topped 3 million, coupled with a decline in exports to the U.S., signals a weakening economic outlook that could further complicate refinancing efforts. The European Central Bank’s reluctance to intervene aggressively to stabilize the bond market adds to the uncertainty, leaving Germany vulnerable to potential liquidity issues and increased default rates among its SMEs. As such, stakeholders must closely monitor these developments, as the interplay of rising yields, political instability, and economic stagnation poses a significant threat to Germany’s financial stability and market access.

Peak Negative Sentiment Narrative - Date: 15-09-2025

Germany is currently facing significant refinancing risks in real estate and broader economic challenges, as highlighted by a series of concerning news reports from August and September 2025. The Bundesbank’s refurbishment project has encountered substantial cost overruns, coinciding with a period of massive losses attributed to prolonged zero interest rates and extensive bond purchases by the European Central Bank (ECB), raising alarms about financial stability. Concurrently, the German government is grappling with rising borrowing costs, with 30-year yields surpassing 3%, the highest since 2011, driven by plans to increase infrastructure and defense spending. This shift towards higher debt levels has raised concerns among economists about a potential transition from long-term to short-term debt, increasing vulnerability to interest rate fluctuations. The economic backdrop is further strained by a rising unemployment rate, which recently exceeded 3 million for the first time in a decade, reflecting a stagnant labor market and declining consumer confidence. The combination of these factors—cost overruns, increased borrowing costs, and a deteriorating job market—signals a precarious financial landscape for Germany, with implications for its real estate sector and overall economic growth. As the country navigates these challenges, stakeholders must remain vigilant to the evolving risks and consider strategic adjustments to mitigate potential fallout from rising refinancing pressures and market instability.

Cross-Country Comparison

Creates comparative visualizations of risk scores across countries, showing aggregated exposure to different risk channels identified in the thematic analysis.

Export Results

Save all generated datasets (labeled results, risk scores, daily indicators, country rankings) to CSV files in the output folder for further analysis or reporting.Conclusion

The Rising Bond Spread Risks workflow provides a comprehensive framework for identifying and quantifying sovereign exposure to bond market vulnerabilities and financial contagion across Western Europe. By leveraging advanced information retrieval and LLM-powered analysis, this workflow transforms unstructured news data into actionable sovereign risk intelligence. Through the automated analysis of bond spread spillover risks, you can:- Identify vulnerable countries - Discover which Western European nations face the highest exposure to bond market pressures through their debt structures, fiscal positions, and market sentiment

- Compare across countries - Understand how different European markets are affected by bond spread pressures, enabling geographic diversification and hedging strategies

- Assess contagion risks - Understand how bond market stress in one country can create spillover effects across the Eurozone, enabling proactive risk management

- Track risk evolution - Monitor how country exposure changes over time as bond yields fluctuate, fiscal conditions evolve, or political dynamics shift

- Generate investment insights - Use risk exposure scores to inform sovereign bond positioning, duration management, and cross-country relative value strategies in European fixed income markets

- Support risk management - Provide quantitative backing for credit risk committees, sovereign exposure decisions, and portfolio stress testing